The Great Software Reset of 2026

-Fed 23, 2026

When Prices Fall First and Stories Follow

Only mAI, Market Mechanics, and the Misunderstood Fear of Commoditization

Only months ago, software stocks were among the clearest beneficiaries of the artificial intelligence narrative. Investors assumed AI would accelerate digital transformation, expand software usage, and create a new wave of productivity across industries. Valuations reflected that optimism.

In just a few months that perception changed radically.

Across the software sector, valuations have compressed sharply. Companies that once traded at premium multiples now sit at levels more commonly associated with mature businesses. Some SaaS firms now trade near single-digit EBITDA multiples, while even the highest-quality franchises command dramatically lower valuations than they did only a year ago.

At first glance, the explanation appears straightforward: investors increasingly fear that artificial intelligence will commoditize software itself. If machines can write code, build applications, and automate development tasks, then perhaps the tools surrounding software development lose their economic value.

Yet this interpretation may misunderstand where complexity — and therefore value — actually resides.

The recent reset in software valuations reflects not only evolving technology risks but also the powerful influence of market mechanics and investor positioning rather than a broader rethinking of how AI reshapes the economics of knowledge work.

A Real Multiple Reset

Part of the decline is undeniably fundamental.

The macro environment has changed meaningfully since the era when growth alone justified premium valuations. Interest rates remain structurally higher, increasing discount rates applied to long-duration assets such as software companies. At the same time, investors have become more selective, rewarding profitability, cash generation, and durable competitive positioning rather than expansion at any cost.

Artificial intelligence has also introduced genuine uncertainty. If AI reduces the cost of writing software dramatically, investors must reconsider which parts of the software ecosystem retain durable value.

These forces have produced a legitimate multiple reset. The era of routinely paying 20–30× EBITDA for high-growth software businesses has given way to a regime where even best-in-class companies often trade closer to mid-teens multiples.

But while these fundamental shifts explain the direction of the move, they do not fully explain its speed or magnitude.

The Scale of the Valuation Compression

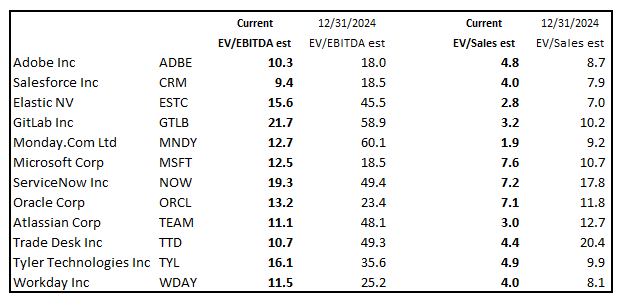

The magnitude of the reset becomes clearer when examining valuation multiples across a range of leading software companies.

In many cases, valuation multiples have compressed by 50–70 percent in a remarkably short period of time. Companies that once commanded premium “AI beneficiary” valuations now trade at levels historically associated with mature enterprise software providers.

Importantly, this repricing has not been limited to speculative names. The compression spans developer platforms, enterprise workflow software, and some of the most entrenched technology providers in the world.

Such widespread declines suggest that the market is applying a broad discount to the entire software ecosystem, reflecting uncertainty about how artificial intelligence may reshape the industry.

The Technical Cascade

The sharpness of the software decline looks more technically driven that fundamental.

Software had become one of the most crowded trades of the AI cycle. Hedge funds, growth managers, and systematic strategies accumulated exposure to many of the same companies. When price momentum softened, this crowded positioning began to unwind.

Systematic strategies amplified the move. Momentum funds, CTAs, and volatility-targeting portfolios respond to price behavior rather than discretionary conviction. As trends deteriorated, these strategies reduced exposure automatically, creating mechanical selling pressure.

Discretionary investors followed similar signals. Broken support levels, widening drawdowns, and rising volatility triggered portfolio adjustments. The process became reflexive: price declines prompted selling, which in turn accelerated price declines.

In such environments, valuation compression can move faster than changes in operating fundamentals would justify.

When Fear Follows Price

One of the most striking features of the recent selloff is the sequencing of investor psychology.

The dominant explanation for software weakness — that AI will commoditize software development — gained prominence only after valuations had already begun to contract. As prices fell, investors constructed narratives to explain the decline: AI might eliminate developers, coding tools might become interchangeable, and software companies might struggle to maintain pricing power.

These concerns are not without merit. Yet markets frequently develop explanatory narratives after price movements have already begun. What appears to be a fundamental reassessment may, in part, reflect investors rationalizing shifts driven initially by flows and positioning.

Fear, in other words, often emerges alongside price declines rather than preceding them.

The AI Commoditization Debate

The current anxiety surrounding software rests on a simple premise: if AI can produce software output cheaply, then software tools themselves may lose value.

But this reasoning may stop too early in the value chain.

Artificial intelligence dramatically lowers the cost of producing digital artifacts — code, reports, models, or data outputs. Yet producing artifacts is only the first step in the lifecycle of modern digital systems. What follows remains both complex and essential: testing, security validation, integration, deployment, monitoring, compliance, and long-term maintenance.

In fact, widespread adoption of AI may dramatically increase the volume of these artifacts. If machines generate code faster than humans ever could, the need to validate, secure, and orchestrate that output grows proportionally.

The consequence is a paradox. AI may commoditize certain forms of creation while simultaneously increasing demand for the systems that manage and govern what has been created.

The Real Disruption: Labor, Not Infrastructure

The more likely economic pressure from AI may fall not on software infrastructure but on portions of the labor market.

For decades, knowledge industries relied heavily on human effort to produce analysis, software, research, and documentation. Artificial intelligence increasingly automates these tasks. What becomes scarce, however, is not the generation of output but the ability to evaluate, interpret, and verify it.

Organizations will continue to depend on software systems to manage the complexity created by AI-driven productivity. At the same time, the role of human workers may evolve toward higher-order judgment: determining which outputs are reliable, identifying errors, ensuring compliance, and interpreting data in meaningful ways.

Rather than eliminating software, artificial intelligence may compress parts of the labor market while increasing the importance of the systems that coordinate increasingly automated workflows.

Infrastructure Software in Practice: The Case of ServiceNow

To see how this dynamic plays out inside real organizations, consider ServiceNow.

ServiceNow sits at the center of critical enterprise workflows — IT service management, security incident response, employee onboarding, procurement approvals, and countless other operational processes. In many companies, thousands of internal tasks flow through the platform each day.

Once deployed and customized, systems like ServiceNow become deeply embedded in an organization’s operational infrastructure. Replacing them would require rebuilding years of workflow automation, retraining employees across departments, and risking disruptions to essential processes.

Artificial intelligence does not diminish the importance of these systems. If anything, it increases it.

As AI tools generate more data and automate more decisions, organizations need platforms capable of orchestrating those actions. Automated processes still require approvals, audit trails, compliance checks, and integration with existing systems. Workflow infrastructure becomes the control layer through which automated activity passes.

In this sense, the value of platforms like ServiceNow lies less in producing output and more in managing complexity. Artificial intelligence may expand the scale of automated work inside organizations, but that work still needs to be organized, governed, and monitored.

Infrastructure in the Age of AI

Technological transitions often follow a similar pattern.

The internet reduced the cost of distributing information but increased the value of platforms capable of organizing it. Mobile computing expanded connectivity while rewarding ecosystems that coordinated millions of devices and applications.

Artificial intelligence may follow the same trajectory.

By lowering the cost of creating digital outputs, AI increases the scale at which organizations operate. That scale requires governance, orchestration, and infrastructure. Rather than eliminating software, AI may shift value toward platforms that manage increasingly automated workflows.

From this perspective, the current anxiety surrounding software may represent less a destruction of value than the early stages of a sorting process between companies built on durable infrastructure and those built primarily on surface functionality.

Opportunity in the Reset

The recent software correction therefore reflects several forces operating simultaneously.

A genuine multiple reset driven by higher interest rates and changing investor preferences. A technical unwind of crowded positioning across growth equities. And a narrative shift fueled by uncertainty surrounding artificial intelligence.

What it does not yet represent is a collapse in the fundamental role software plays inside modern organizations.

Revenue growth across many software companies remains healthy. Margins continue to expand. Balance sheets are generally strong. The gap between business performance and market pricing suggests that sentiment and market mechanics have contributed meaningfully to the current valuation landscape.

Periods like this often produce the most interesting opportunities.

When uncertainty rises and narratives shift rapidly, markets frequently overshoot. Investors must distinguish between companies whose value is genuinely threatened by technological change and those whose importance may actually increase as complexity grows.

The Pattern Markets Repeatedly Follow

Market cycles often unfold in a familiar sequence.

A powerful technological narrative attracts capital and concentrates positioning. Expectations rise quickly. A reversal in price momentum triggers mechanical selling and risk reduction. Narratives evolve to explain the decline. Fear expands.

Eventually, fundamentals reassert themselves.

The current software reset appears to be navigating this pattern in real time. Prices fell first. Stories followed. Uncertainty expanded.

And within that process lies the deeper question investors must answer — not whether artificial intelligence disrupts software, but which parts of the software ecosystem become indispensable in an AI-driven world.