A Smarter Path for U.S. Healthcare: Borrowing Discipline from Singapore Without Losing American Choice

-Sept 12, 2025

The U.S. Paradox

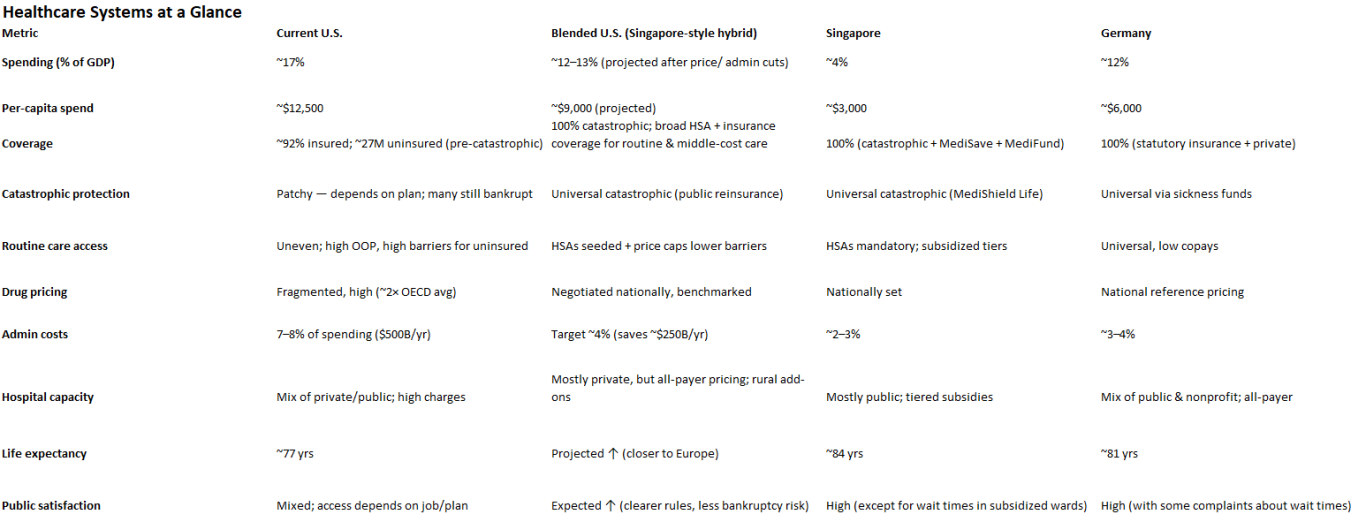

America spends more on healthcare than any country on earth. At nearly 17% of GDP — about $12,500 per person — our system costs almost twice as much as Germany’s and more than four times what Singapore spends. Yet tens of millions remain uninsured or underinsured, medical bankruptcies are common, and life expectancy lags peers.

The question isn’t whether U.S. healthcare needs reform — it does. The real question is whether we can build a system that both lowers costs and broadens access in a uniquely American way.

Why We Must Get It Right the First Time

America’s history with big social programs shows one clear pattern: once created, they rarely get unwound. Social Security, Medicare, Medicaid, and the Affordable Care Act were all controversial when passed. Yet each became embedded in the political and social fabric, effectively irreversible.

That permanence is not a comfort — it’s a warning. If the U.S. takes on another sweeping healthcare reform, we cannot afford to experiment recklessly or design something shortsighted. A program that is politically impossible to reverse must be fiscally disciplined, structurally sound, and adaptable for decades to come.

The goal isn’t just to solve today’s problems of high cost and spotty access. It’s to build a system smart enough to withstand demographic shifts, economic shocks, medical innovation, and political change. In other words, the reform we adopt will be the one our children inherit — so it must be designed to last.

Lessons from Abroad

Other nations prove it’s possible to achieve better outcomes for less.

Singapore: Spends ~4% of GDP on healthcare, yet delivers life expectancy near 84 years and infant mortality among the lowest in the world. Its formula: catastrophic coverage for all (MediShield), mandatory health savings accounts for routine care (MediSave), and strict national price regulation.

Germany: Spends ~12% of GDP, covering everyone through competing nonprofit sickness funds, all-payer rate-setting, and mandatory participation.

United States: Spends ~17% of GDP, with high fragmentation, rising hospital and drug costs, and nearly 30 million left outside the system.

Singapore is too small, too dense, and too disciplined to copy outright. But its principles — catastrophic backstop, savings responsibility, and price discipline — are portable. Combined with Germany’s universality and America’s tradition of choice, they point toward a workable hybrid.

A Blended U.S. Model

1. AmeriShield (Public Catastrophic Coverage) Every American is automatically covered for catastrophic costs. A national reinsurance layer, funded by payroll and consumption taxes, takes million-dollar cancer treatments or trauma bills off the shoulders of families and private insurers.

2. MediSave-US Accounts Modeled on Singapore, but adapted: every worker is auto-enrolled in a health savings account. Employers can contribute, the government matches for low- and middle-income families, and balances roll over year to year. These accounts pay for routine doctor visits, prescriptions, imaging, and deductibles.

3. All-Payer Price Schedules Hospitals and drug companies face a national fee schedule, just as Germany and Japan use today. The same MRI costs the same whether you are insured by Aetna, UnitedHealthcare, or a public plan. Rural and teaching hospitals get add-ons to protect capacity.

4. Private Insurers as Middle Layer Insurers cover the “middle band” of expenses — the zone between routine care and catastrophic costs. This keeps private players in the game, competing on service instead of cherry-picking risk.

5. Tiered Amenities, Not Access Everyone receives the same medical care. But patients can pay extra (or use supplemental insurance) for private rooms, faster elective surgery, or hotel-like amenities. This respects American expectations of choice without creating unequal access to essential care.

6. Primary-Care First All plans must spend a minimum share on primary care. Capitation and quality bonuses replace fee-for-service churn. Same-day or next-day access becomes the national standard.

Immigration and the Cost Burden

No reform can ignore immigration. U.S. law (EMTALA) requires hospitals to stabilize anyone in an emergency. That means undocumented immigrants already generate billions in uncompensated care, costs that fall heavily on border states and urban hospitals. Singapore’s solution is simple: non-citizens pay unsubsidized rates, and foreign workers must carry insurance. The U.S. is more complicated, but the principle applies.

Emergency stabilization must remain — both legally and morally.

Federal reimbursement pool: Hospitals treating undocumented patients should be made whole through a national fund, financed by a mix of remittance fees, visa surcharges, and penalties on employers who hire off the books

Legal entrants carry insurance: As in Europe, visas should require proof of coverage.

Direct billing of foreign governments is unrealistic — there are no treaties or enforcement mechanisms. But cost-offset tools can prevent frontline hospitals from bearing the full weight.

This ensures border hospitals stay solvent, taxpayers know where the money comes from, and costs are contained.

A Family-Level View

Take a median-income family of four:

Today: They may pay $20,000 in premiums, face a $6,000 deductible, and risk surprise bills even after insurance. Catastrophic illness could still bankrupt them.

Blended Model:

Premiums drop because catastrophic risk is socialized.

Their MediSave-US account is funded by payroll contributions, employer match, and federal seeding.

Routine care comes from their account at transparent prices.

If cancer strikes, AmeriShield takes over after the insurer pays up to the threshold. No bankruptcy, no uncertainty.

This is not theory — it’s what Singaporeans already experience, at one-third the U.S. cost.

The Politics of Possibility

A reform of this scope has to cross party lines:

Left: Universality, fairness, end of medical bankruptcy, price discipline.

Right: HSAs, personal responsibility, private insurance preserved, no full single-payer.

Center: Lower costs, broader access, and realistic implementation in phases (0–2 years: catastrophic backstop and price schedules; 2–5 years: seeded HSAs and primary care standards; 5–10 years: expand and refine).

This isn’t a utopia. It’s a blueprint for a coalition.

The Choice Before Us

The U.S. faces a stark decision: cling to the most expensive system in the world with patchy outcomes, or adapt proven international lessons in an American way.

We don’t need to choose between chaos and single-payer. By blending Singapore’s thrift, Germany’s universality, and America’s tradition of choice, we can finally achieve what everyone claims to want: lower cost and broader access. History shows reforms become permanent. The question is whether we will lock ourselves into a bloated, unsustainable status quo — or seize the chance to build a system smart enough to last for generations.