A Pattern of Mortgage Hypocrisy: James, Cook, and Schiff Show How Elites Bend the Rules

-Sept 4, 2025

In recent months, three of America’s most prominent public officials have come under federal investigation for the same basic offense: misrepresenting mortgage documents to gain financial advantage. New York Attorney General Letitia James, Federal Reserve Governor Lisa Cook, and Senator Adam Schiff each deny wrongdoing. Yet none deny the facts on paper. Each signed certifications that don’t square with reality. Each benefited financially. And each now insists it wasn’t fraud but politics.

Letitia James: “No One Above the Law” — Except Herself

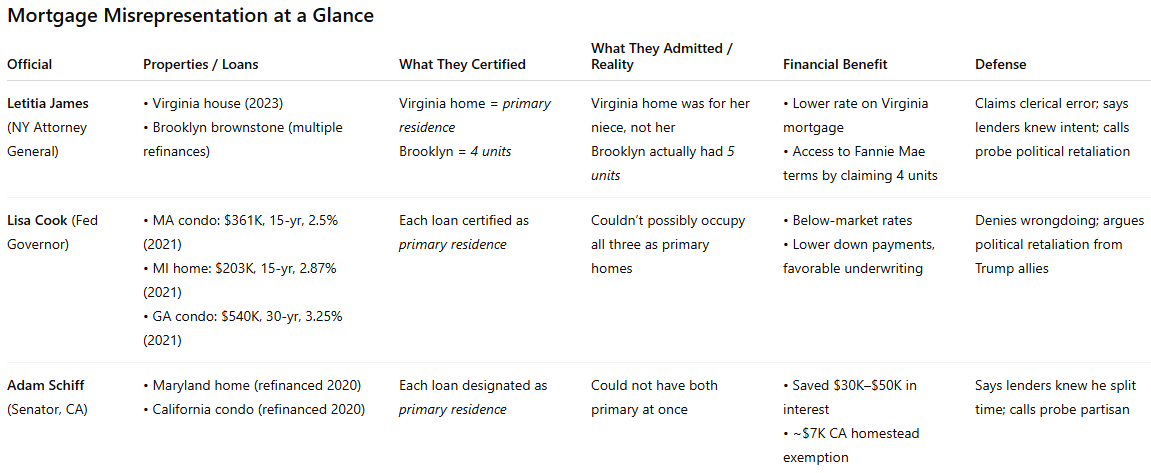

James built her career prosecuting Donald Trump with the mantra that “no one is above the law.” Yet she signed a sworn certification that a Virginia property was her primary residence, later admitting it was for her niece. At the same time, her Brooklyn brownstone carried a city certificate for five units but appeared as four on multiple mortgages — the difference between costly commercial financing and cheaper Fannie Mae terms.

The facts are simple:

She signed the primary residence affidavit.

She admitted it wasn’t her home.

She understood the benefits, from occupancy rules to unit counts.

As a lawyer and Attorney General, she cannot claim ignorance.

What she once called fraud when Trump did it, she now calls clerical error.

Lisa Cook: The Fed’s Mortgage Problem

Cook faces a Justice Department probe into three different loans she signed in 2021:

A $361,000, 15-year loan at 2.5% in Massachusetts.

A $203,000, 15-year loan at 2.87% in Michigan.

A $540,000, 30-year loan at 3.25% in Georgia.

Each loan carried the same certification: this is my primary residence. Only one could be true. Each designation gave her lower rates and lighter terms.

As a Federal Reserve Governor, Cook sits at the heart of the very system she allegedly gamed. The Fed buys trillions in Fannie Mae and Freddie Mac securities. For her to misstate occupancy is not a layperson’s mistake — it is a central banker taking advantage of rules she knows intimately.

Adam Schiff: Double Primary, Double Standard

Schiff, the impeachment manager who insisted on Trump’s accountability, refinanced both his Maryland home and California condo in 2020 — each time as a primary residence. He saved tens of thousands in interest and picked up homestead exemptions along the way.

Like James and Cook, Schiff doesn’t deny the filings. He says lenders knew he split time, and that politics drives the investigation. But mortgage law is not based on lifestyle interpretation. One primary residence means one — not two. As a lawyer and longtime Congressman, Schiff knew that.

The Common Thread

James, Cook, and Schiff tell different stories but share the same pattern:

They signed certifications under penalty of perjury.

They profited financially from favorable terms.

They had ample opportunity to correct the record.

And now they argue that it wasn’t fraud but politics.

That is hypocrisy. What they condemned in others they excuse in themselves.

Why It Matters

The issue isn’t just personal credibility. It’s institutional trust. James runs the top law enforcement office in one of America’s largest states. Cook sits on the board of the nation’s central bank. Schiff writes the laws the rest of us live under. If they can treat mortgage rules as flexible suggestions, while insisting that ordinary citizens follow them to the letter, then no one is above the law becomes an empty slogan.

The lesson is stark. Law without equal application is not law at all — it is power. And when those who benefit most from the system bend it for themselves, public trust collapses faster than any housing market bubble.

Additionally

When confronted with allegations that she misrepresented her niece’s home as her own primary residence and undercounted units in Brooklyn, New York Attorney General Letitia James has denied intent to defraud. She has leaned on clerical-error explanations and called the investigations political.

But the problem goes deeper than paperwork. In a recent Nation profile, James was quoted declaring: “We have to stop believing or following the rules. Break the rules. Stop coloring inside the lines.”

For an activist, that line might be a rallying cry. But for a state’s top law enforcement officer — the one who prosecuted Donald Trump’s organization for misstatements in loan documents — it’s a confession of worldview. The rules apply when she enforces them against others. They’re optional when they constrain her.

And that is what corrodes institutions. If the chief law enforcer believes rules are tools to be bent rather than standards to be upheld, then the law itself becomes suspect.